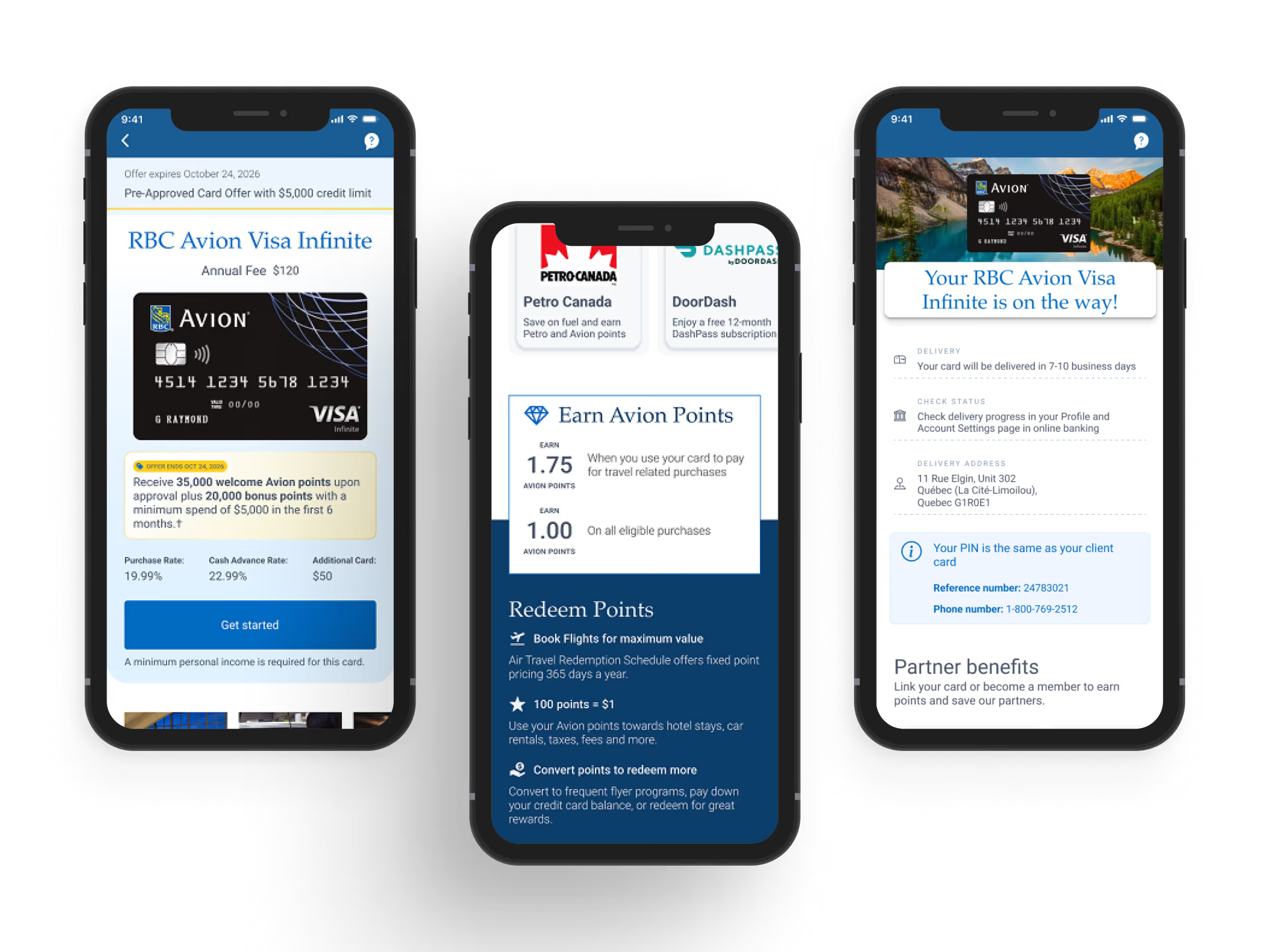

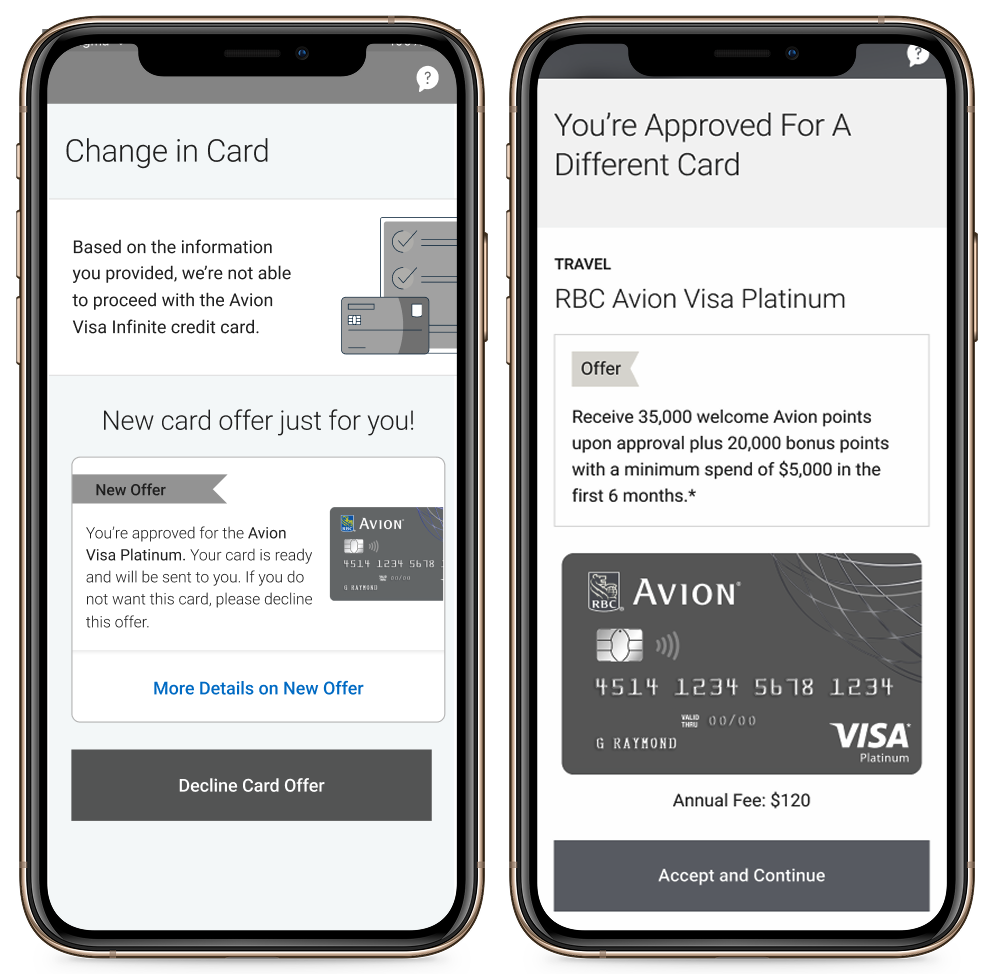

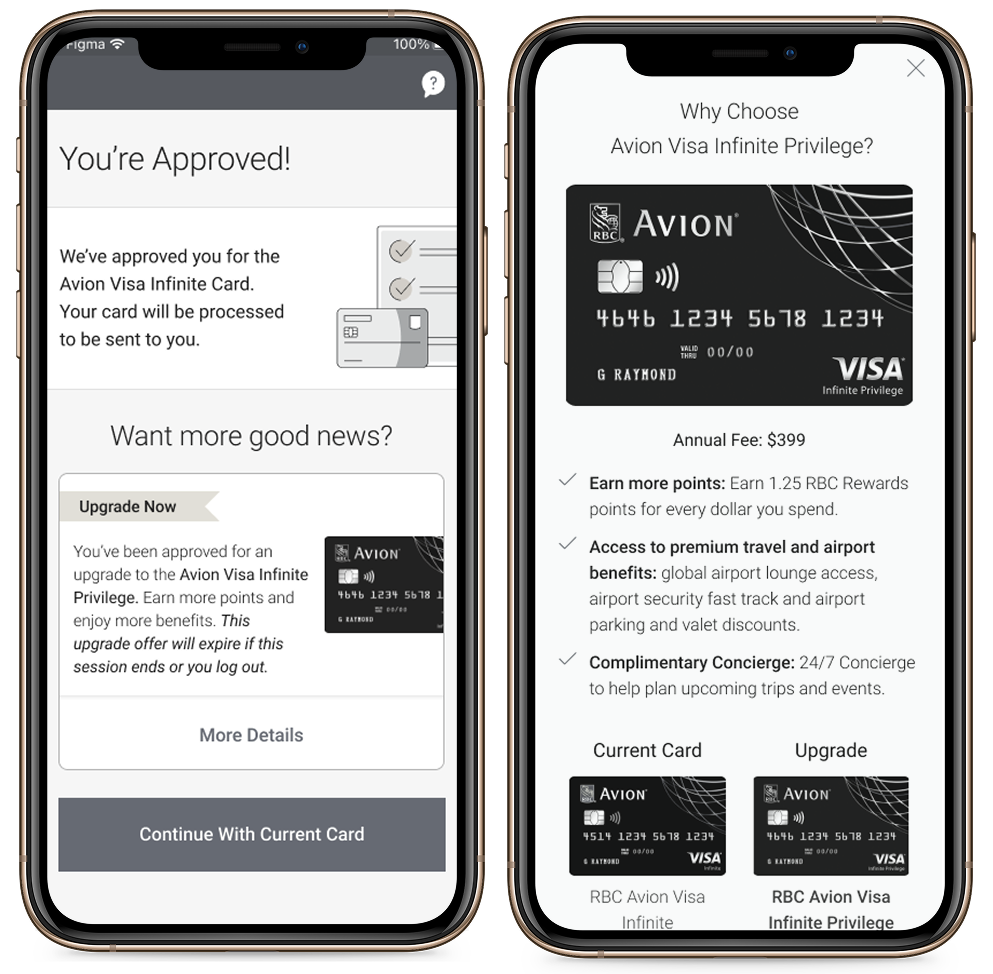

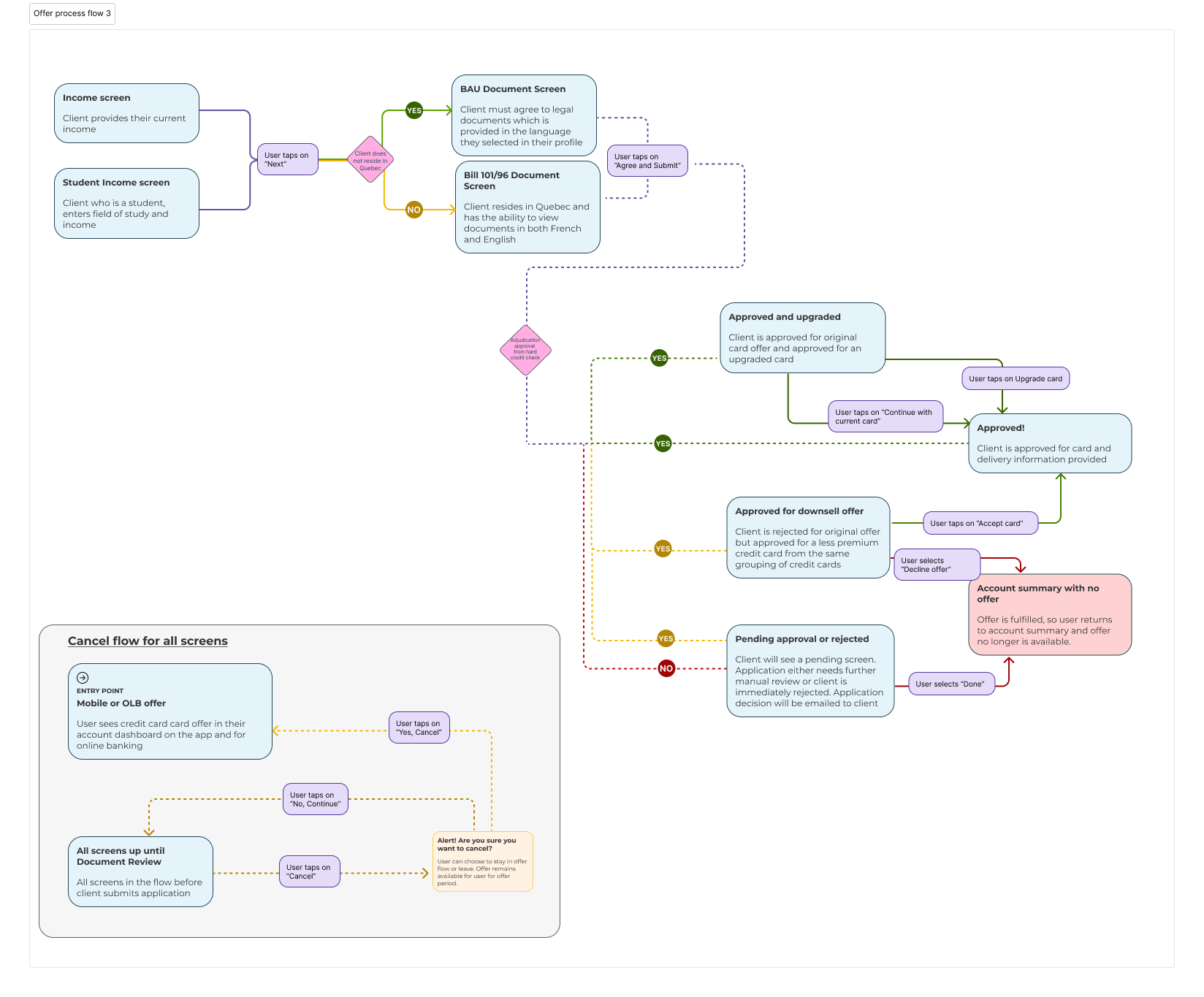

In initial testing, users were very confused by the "Upsell scenario", which is a more premium card provided to clients who shared a higher income and/or a better credit score than on record.

Were they still eligible for the original card? Understanding this new path also required learning all about a new product, something they already mentioned in user testing as not being ideal.

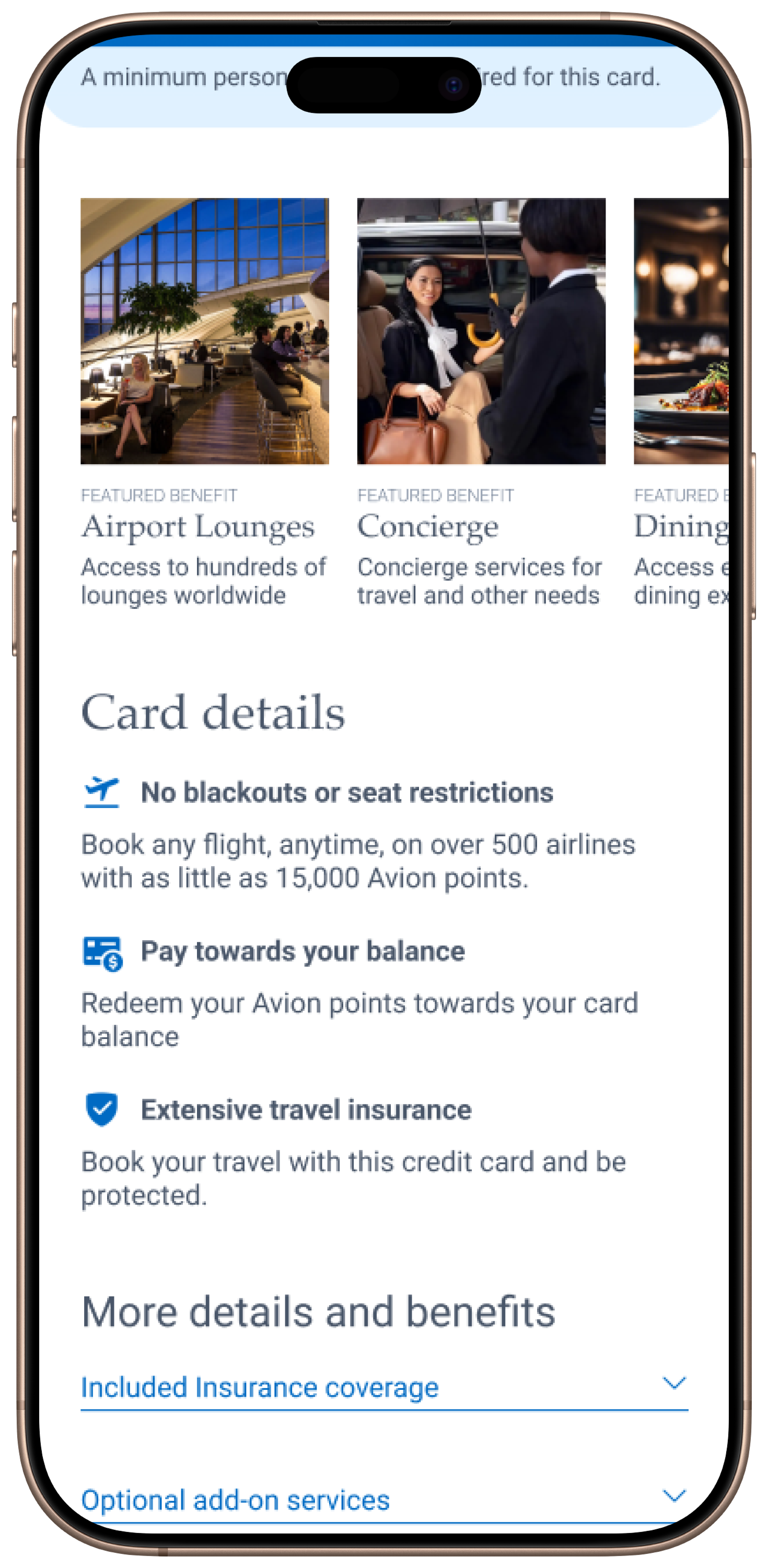

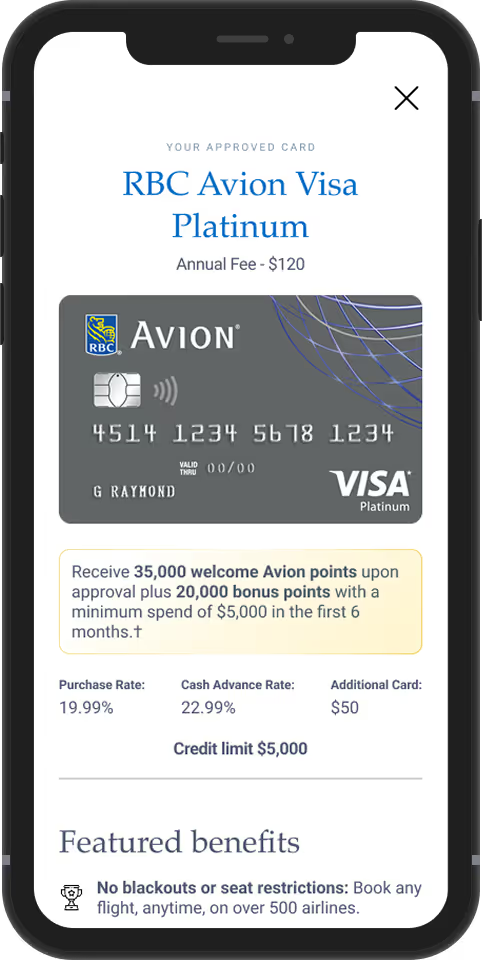

Upsell screen acknowledges their approval and visually forces the client to choose - with the use of radio buttons - between the original card or the upgraded card. Clients are able to view the product page, which includes a compare chart for both card options.

Prototype for this experience

{kind=link}

{kind=link}

{kind=link}